US Healthcare's Persistent Inflation Robs the Economy of Productive Resources

When you really need a health intervention, price is not your priority.

The healthcare sector in the United States has developed keen market instincts and has been rewarded with an ever-increasing piece of the overall economic pie, which, as of 2023, reached 17.6% of GDP. With the discovery of pricing power, the sector has become accustomed to significant annual price increases, a dynamic that is very hard to break. The additional money finds its way to all corners of the healthcare system, from doctors and administrators, to drug and device makers, insurers, lobbyists and all sorts of industry middlemen, making it extremely challenging to come up with a simple solution to the problem. There is no main culprit, and no true villain that is responsible for the runaway cost issue. Instead, it is a systemic failure, where the industry takes an ever-increasing proportion of the country’s resources for one simple reason: because it can.

What enables the healthcare sector to continually demand price increases above the country’s level of inflation?

It is the nature of the services it provides.

The consequences of not addressing a serious health condition are something between a greatly diminished quality of life and death. While cost matters, it is not the priority. This gives the sector great pricing power.

The US runs a market-based system in healthcare, where the countervailing forces are supposed to determine clearing prices. The providers (hospitals, doctors, drug companies) are on one side; and the payers (insurance, Medicare), employers (who pay for health insurance) and individuals on the other. The outcome has been ever-increasing prices, making it clear which side has most of the negotiating leverage.

80% of Americans say they are dissatisfied with healthcare costs. In 2023, health expenditures totaled $14,750 per person, a 7.5% increase over 2022. Inflation was 3.4%. The US spends 50% more per capita on healthcare than any other rich Western country, and twice as much as Japan and the UK, for example.

Source: OECD

This dramatic differential has been growing since 1980, when US spending was somewhat closer to that of comparable countries. Between 1997 and 2012, for example, the cost of a hospital stay rose 149% in the US, while the cost of physician services was up 55%. Inflation for that period was 43%. Today, in dollar terms, a hospital stay in the US costs 3 times as much as one in Australia and 10 times more than one in Spain.

Source: OECD, Commonwealth Fund

The primary difference between the US healthcare system, and that of most other rich countries is the lack of a large, central payer which negotiates and sets prices for the entire system. Other countries have recognized that allowing the market to set prices for health treatments has serious shortcomings. Americans, in contrast, with their lack of trust in government and embrace of free markets, have given healthcare players freedom to discover what prices the market will bear. The result is high prices for the same procedures, consults, drugs and devices. The table below shows what procedures cost in other countries as a percentage of the US cost, as of 2022:

Source: Health Care Cost Institute

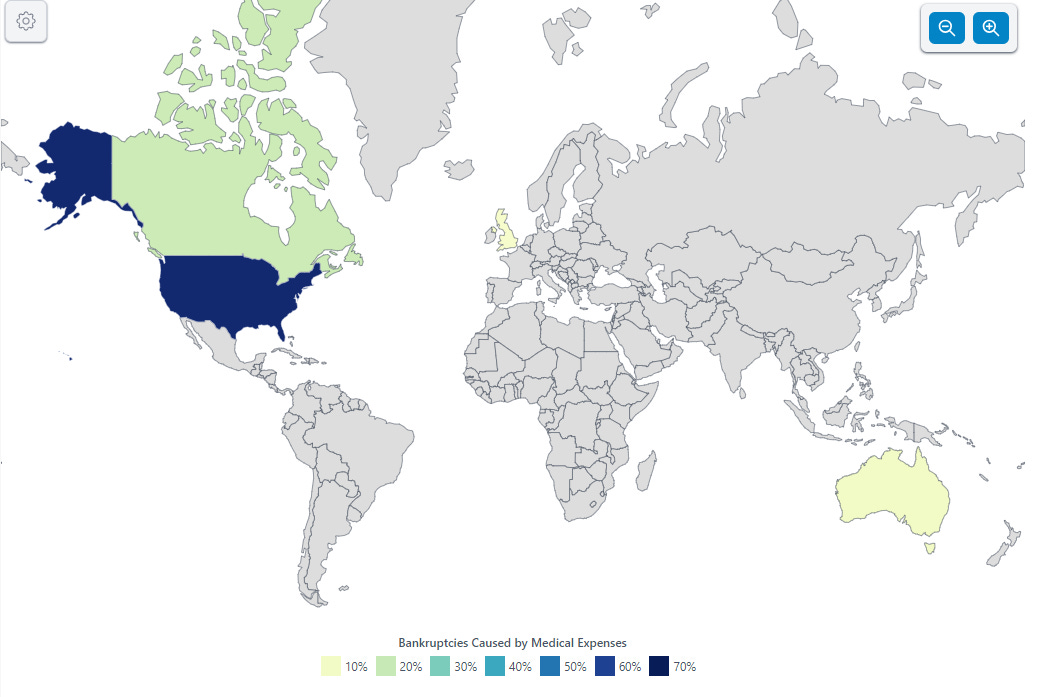

In 2023, 89% of Americans had some form of health insurance. Even among the insured, however, many experience serious financial strain related to healthcare costs. 41% of adults in the US have debt from medical expenses, and about half of them say they are unsure if they will ever be able to pay it off completely. 1 in 7 of those with medical debt say they have been denied medical treatment because of unpaid bills. Medical debt is the largest cause of personal bankruptcy in the US, with approximately 530,000 families filing for this reason every year.

Percentage of Personal Bankruptcies Caused by Medical Expenses, 2024

Source: World Population Review

The US healthcare system delivers its services with decent quality. There is, by and large, a reasonable supply of competent doctors, nurses, and other practitioners to attend to the country’s needs. Facilities are plentiful, with some areas oversupplied, and generally modern and well equipped. Standards of care are high by almost any global standard. The most advanced techniques, devices and treatments are widely available.

Source: The Commonwealth Fund

Americans, according to surveys, tend to be pretty happy with their healthcare coverage. In a recent poll of Americans covered by employee-sponsored insurance plans, 71% of respondents said the quality of their plans was high, and 76% thought their plan would cover major expenses in a major medical emergency. Given the medical debt statistics above, we can see this belief is incorrect (55% of Americans receive employer-based health insurance). Nonetheless, many Americans are reticent to demand any major overhauls that may risk a deterioration in the benefits they currently receive. In healthcare, people don’t want to rock the boat.

Each part of the US healthcare system has discovered pricing power and been exploiting it, as expected in a market system. Along the way, the different players have developed a healthy taste for constantly increasing revenues. Much of the American health system is non-profit, at least nominally, yet even these entities exhibit the same revenue maximizing behavior as their for-profit brethren. The techniques to achieve this are numerous and constantly evolve.

Source: American Hospital Association

As things stand today, the cost of most key inputs into medical care are already higher in the US than they are in comparable countries. Physician and administrative salaries are higher in the US than elsewhere.

Source: Statista

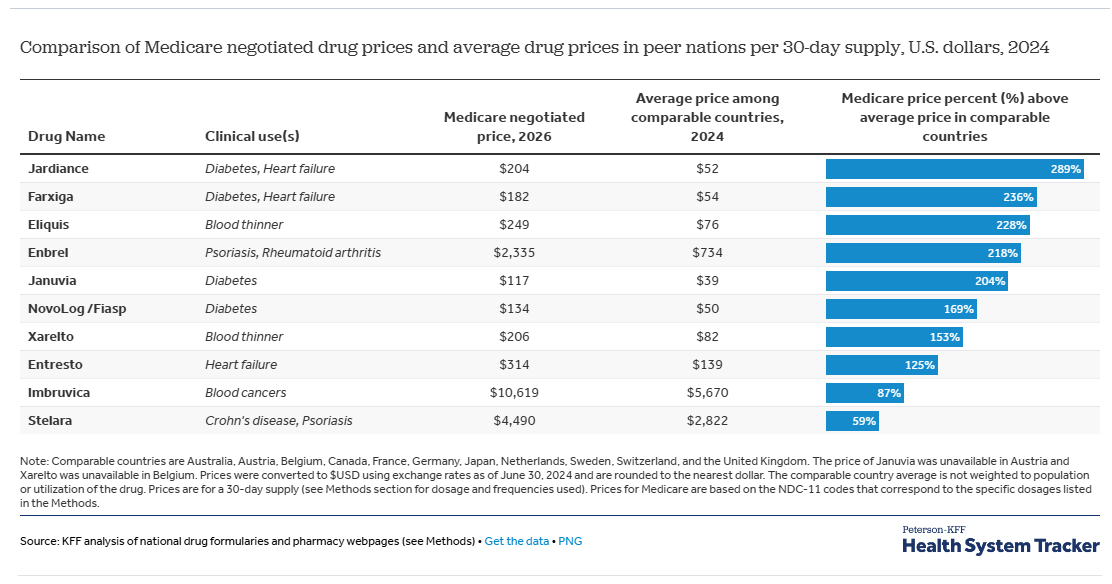

Pharmaceutical companies have learned they can price aggressively in the US and gotten bolder over time. They tend to introduce drugs at a high price point, increase prices over time, and have got in the habit of removing cheaper drugs from the market (to force the purchase of costlier ones). Americans pay, on average, 2.8x the price for drugs when compared to other rich countries (this is a like-for-like comparison, using the prices Medicare pays in the US as a reference). Even for the few drugs Medicare is allowed to negotiate prices for, presumably the best deals Medicare has extracted, premiums to international prices range from 59% to 289%.

Source: Health System Tracker, KFF

Hospitals incentivize doctors with “productivity bonuses” that reward those whose interventions generate more revenue per patient. They are encouraged to order more expensive tests, higher numbers of them, and sometimes recommend more costly procedures that may not be needed or be the optimal course of action. This is not to say that doctors are crooks. Most are not. Yet they are often incentivized to make decisions that maximize revenues, and feel they are in a gray area where the patient is not harmed by having extra lab tests or a more expensive procedure.

Upcoding, the practice of billing insurance for higher level interventions, even when the interventions have been of a lower order with the intention of receiving higher payments, has also become common. A 2012 study by the Center for Public Integrity showed how the majority of American emergency rooms’ claims went from low level interventions (level 1, 2 and 3) in 2001 to high level (level 4 and 5) by 2008.

Medical device makers have also got in the game. Companies whose equipment has become “standard of care” for a particular use, will frequently introduce new versions of existing devices at higher prices and discontinue cheaper versions. Often times, the new devices do not produce any substantial improvements in outcomes.

Hospital networks have been consolidating aggressively to gain market power in their regions. There were 1,573 hospital mergers from 1998 to 2017 and another 428 hospital and health system mergers from 2018 to 2023. By 2022, 68% of community hospitals were part of a larger health system. This gives them the ability to negotiate better rates with private insurers and increase their revenues. Hospital systems cite the need for efficiency in their push to consolidate. Studies have shown that cost savings average between 3 and 4% after mergers and takeovers, yet price increases at newly consolidated hospitals tend to accelerate significantly after the deals, averaging between 40 and 50%.

Source: KFF

Price opaqueness has emerged as one of the principal tools the industry uses to manage prices and keep them high. In a 2022 survey, only 17% of patients who tried were able to obtain pricing for services before they were administered. Hospitals are notorious for charging dramatically different prices for the same services, depending on what the patient’s coverage policy allows them to get away with. Prices among hospitals in proximity to each other can also vary widely, even when dealing with the same payers. This is because insurance companies negotiate separately with each hospital provider, and the complexity of the negotiations and service offerings create plenty of opportunities for inconsistency. In addition, some providers have significant market power in certain areas, and can demand higher prices from the insurers. Insurers could decide to exclude these expensive providers from their networks, yet seldom do as their policyholders want access to those dominant providers. The solution, instead, is to pass on the extra cost in the form of higher policy costs.

The pharmaceutical industry has also become expert at casting doubt on what actual realized drug prices are, claiming big buyers negotiate discounts, and those prices are shielded by confidentiality agreements. In addition, they argue that assistance is given to many individuals who can’t afford the treatments, so average prices are not a good way to gauge affordability. Medicare, the largest purchaser of drugs in the country, was prohibited from negotiating drug prices until 2024. It has begun this process meekly, however, tackling only a few drugs each year, and demanding moderate discounts.

The US healthcare system has a strong embedded inflationary impulse, impairing its ability to ever contain costs, and thus price increases. The prices of one segment of the healthcare sector are another one’s costs. As prices go up in one area, it pressures another area to pass this increase onto their customers, and on and on. In the twelve months ended October 2024, for example, US hospital revenues increased 7.5%, yet their businesses were squeezed by their own labor costs (+7%), supply expenses (+13%), service expenses (+13%) and drug expenses (+15%). Hospitals, on average, are not currently making good profits, and some are having financial difficulties. Without a doubt, they are gearing up to increase prices further to restore profitability.

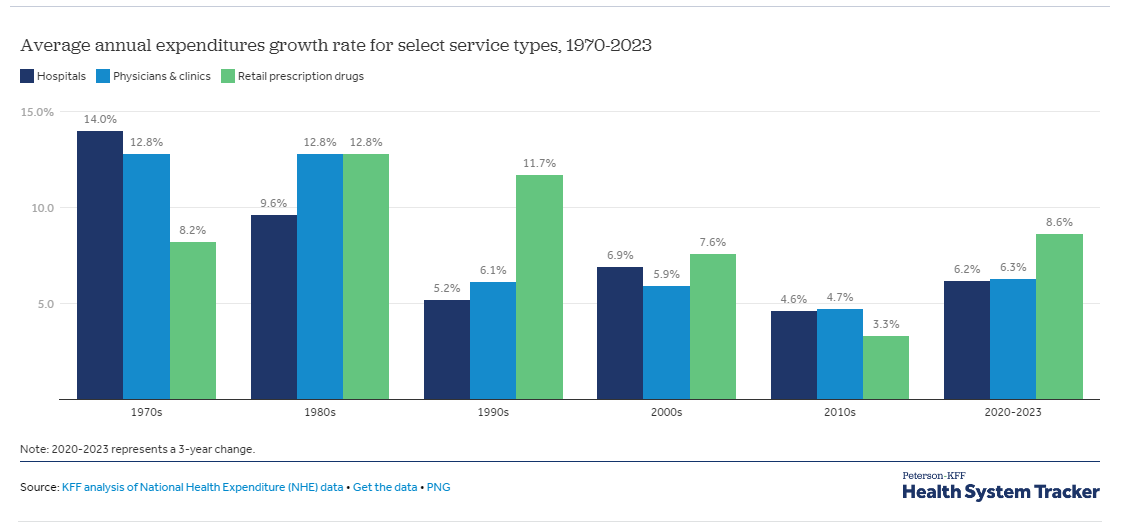

The table below shows the average annual increase in pricing in the healthcare sector, broken down by type. In all of the time periods shown, the increases have significantly outpaced US inflation.

US Healthcare: Average Annual Growth Rates by Expenditure Type

Source: Peterson - KFF Health System Tracker

It is the private insurance companies, together with Medicare, that have the role of trying to keep pricing under control in the system. Federal Medicare and Medicaid spending are responsible for a third of all healthcare payments in the country and therefore have significant negotiating power. The power of health insurers is also material, as the industry has a few big players that dominate in each region. In today’s market, Medicare, with its scale, gets the best deals. Large insurers get the next best prices. Providers then compensate by charging higher prices to smaller insurance companies, and especially to the uninsured.

The dynamic between insurance companies and providers has devolved into a negotiating game where providers try to have the highest possible list prices and insurers attempt to get the highest possible discounts to those. Despite annual bargaining, the overall result has been yearly premium increases for policyholders. At the end of the day, there is a tacit acknowledgment by both parties that the consumer will pay higher prices, and the inflationary dynamic continues as the path of least resistance.

The insurance market also suffers from a lack of competition due to high regional concentration in market share. A 2022 survey of the insurance industry found that 73% of metropolitan statistical areas were “highly concentrated”, with 48% of them having one health insurer with over 50% market share. Clearly this contributes to the industry’s ability to increase prices and pass on the mark-ups that providers are demanding.

All of the features of the healthcare system mentioned above, from higher salaries for medical professionals, to productivity bonuses, consolidation of hospital networks, high drug pricing, and price opaqueness - and many others I did not mention - contribute to medical price inflation. Ultimately, it is individuals who pay for it and do so because they have little negotiating leverage vis-a-vis the providers.

Attempts to introduce regulation to temper the ability of the sector to price freely have often been stunted. The sector employs armies of lobbyists to influence regulatory and legislative action, with significant success. Healthcare spends the most of any industry on lobbying in the US, clocking in at $739 million in 2023 (compare this to $130 million spent by oil and gas and $147 million by the securities industry). When their attempts fail, the sector has generally been able to adapt to new rules and find ways to safeguard their profitability. The problem lies less in the detail of regulation, and more in the overall design of the system.

A solution is not in sight. Perhaps the day of reckoning will come when the major government health programs face insolvency, as Medicare is forecast to do in 2036. More likely than not, healthcare will continue to be a weight on the US economy, sucking resources away from other potential uses, pressuring and stressing businesses and individuals, and continuing its growth through price increases.

Article guide:

Elizabeth Rosenthal: An American sickness: How healthcare became big business and you can take it back.

American Hospital Association: Fast facts on US hospitals 2024.

Peterson-KFF Health System Tracker: How has U.S. spending on healthcare changed over time?

Fierce Healthcare: 2025 Outlook: Hospital finances show signs of stability, but rising costs will be a major headwind.

Center for Medicare and Medicaid Services: NHE fact sheet 2023.

Visual Capitalist: Which US sectors spend more on lobbying?

Retire Guide: General Medical Bankruptcy Statistics.

KFF: Ten Things to Know About Consolidation in Health Care Provider Markets.

The Commonwealth Fund: Mirror, mirror 2024: A portrait of the failing US health system.

Forbes: It turns out Americans really love their healthcare.

American Medical Association: 95% of U.S. health insurance markets are “highly concentrated”.